In a strange twist, during a time of the highest oil prices ever recorded, an oil man is placing the biggest bet of his life on wind, water and natural gas. Earlier this year, T. Boone Pickens placed approximately a $1.3 billion order with General Electric for 667 1.5 MW wind turbines, as the first phase of his 4 Giga Watt Pampa Wind Project in the Texas panhandle. The Pampa Wind Project will be complete by 2014 and will be five time larger than the next largest wind project in the United States. The overall project is expected to entail an investment of approximately $8 billion over the next six years in installing the wind farm. But that's not all...

Mr. Pickens is also overlaying additional investments and initiatives to create valuable synergy across his portfolio of investments. His Pickens Plan is publicly encouraging wind development and the conversion of cars to natural gas. In addition, he has acquired water rights in the same area as his wind farm. His Pickens Plan, presented in the public interest, when coupled with his corresponding wind, water and natural gas investments, could be worth billions in coming years. Below, let's review the magic of Pickens' Synergy.

CREZs - One important innovation aiding Mr. Pickens in his plans is the creation by the Texas Legislature of Competitive Renewable Energy Zones (CREZs) as part of Senate Bill 20. These CREZs address the critical challenge of linking wind resources to the electric grid, with the identification of 25 zones where wind power could be profitably developed, and having the state agree to build transmission lines out to those zones. The panhandle is one of those zones, a critical enabling lynchpin in Mr. Pickens' plans.

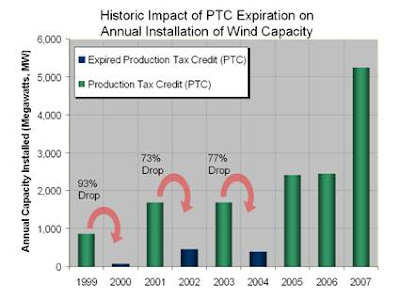

PTC - Mr. Pickens is also very supportive of another source of value for his project, the Wind Energy Production Tax Credit, which is expiring at the end of this year. The PTC is a tax incentive that was created with the Energy Policy Act of 1992 (EPACT 1992). The PTC provides an income tax credit of 2 cents per kWh for electricity produced over a ten year period by qualified wind energy facilities and other renewable projects placed in service after December 31, 1992, and before January 1, 2009. The amount of the tax credit has been adjusted over the years for inflation, with the original credit set at 1.5 cents in 1992.

Over the years since 1992, the PTC has lapsed three times, each with a significant negative impacts on the level of annual wind plant installations, seen in the chart below from teh American Wind Energy Association (AWEA).

The PTC is currently up for renewal in Congress. The House has consistently passed PTC language in several bill, but unfortunately the Senate has had a difficult time of it, holding eight votes on legislation incorporating the PTC, but approving the extension on only one occasion. Apparently, the reason why the Congress has been having a difficult time passing the legislation is not the fundamentals associated with PTC, but it runs counter to a new policy in Congress that requires every spending proposal or tax cut specifically linked either to a spending reduction or a revenue source. Although this policy was broadly instituted by the Democrats, it is the Republicans that are requiring the identification of a counterbalancing source of revenues for the PTC before providing passage. The Democrats in his case are arguing that the PTC is grandfathered in, thus obviating the need for applying the offsetting revenue source.

Water - Pickens has also been buying up water rights in the same area that he is building his wind project, focused in on Roberts County in the northwest portion of the panhandle. His new company Mesa Water, has purchased the ground water rights of 200,000 acres in Roberts County for $75 million, expecting to make $1 billion over the next 30 years. His plan is to take water from the Ogallala Aquifer and pipe it to one or more major cities in Texas, distributing approximately 200,000 acre feet per year. Water below - wind turbines on top. Interesting source of synergy.

Natural Gas - The Pickens plan also is promoting the move to natural gas based vehicles, to address security and economic issues associated with importing petroleum, and to reduce emissions. One cannot overlook, however, that Mr. Pickens, through his investment vehicle BP Capital Holdings, owns stock in nine companies involved in natural gas exploration and production amounting to a stock value of $838 million. Converting 220 million vehicles to run on natural gas would increase natural gas demand by 80% over current demand in the United States of 21.7 trillion cubic feet per year to 39.0 trillion cubic feet. Even if we converted only 25% of our cars to run on natural gas, this would amount to a 20% increase in demand for a resource that is getting harder to find, and one that is increasingly being sourced globally through importation of liquified natural gas.

Summary - In summary, Mr. Pickens remains a very astute business person, even in his eighth decade. He could make a billion dollars off of his wind investment, a billion dollars off of his water investment, and a billion dollars off of his natural gas investment. Not bad for a reformed oil person who has become a clean energy advocate.